English

English  Français

Français HOUSING – IS IT STILL POSSIBLE TO BECOME A HOMEOWNER IN SWITZERLAND?

According to Eurostat statistics, fewer and fewer Swiss residents own their own home; in fact, only one in three Swiss people own their own home.

Switzerland is a nation of tenants. Eurostat’s European statistics confirm this: only Spain and Latvia have a higher proportion of tenants than Switzerland (63.2%) relative to their populations.

Let’s examine, point by point, the various reasons why the Swiss middle class can no longer afford to buy their own homes…

…Let alone invest in buy-to-let property, which would nevertheless represent the surest way for them to secure their retirement.

Retirement has become precarious due to the very serious problems currently facing pension funds, which will worsen in the coming years, to the extent that only those who can demonstrate retirement savings (LPP) in excess of CHF 1,000,000– and a full AVS pension (i.e. approx. 30% of the population) will have a chance of being able to live with dignity in Switzerland in their retirement.

The figures and analysis

One in five Swiss people (22.6%) live in a detached house

One in ten (10.8%) in a terraced house, according to 2017 data.

And the trend is downwards: two years earlier, there were slightly more homeowners, with an extra percentage point in each category.

Nine out of ten residents are tenants in Geneva and Lausanne

Geneva, Lausanne and Zurich are the Swiss cities with the highest proportion of tenants. Nine out of ten homes are occupied by tenants, according to figures published by the Federal Statistical Office (FSO).

Geneva leads the way with a tenant rate of 91.4%, followed by

Lausanne (90.3%)

and Zurich (89.9%)

Nationwide, the proportion of tenants stands at 59%, according to data compiled by the FSO between 2012 and 2016 as part of its federal population census.

In the 174 localities analysed by the FSO, tenants are almost always in the majority.

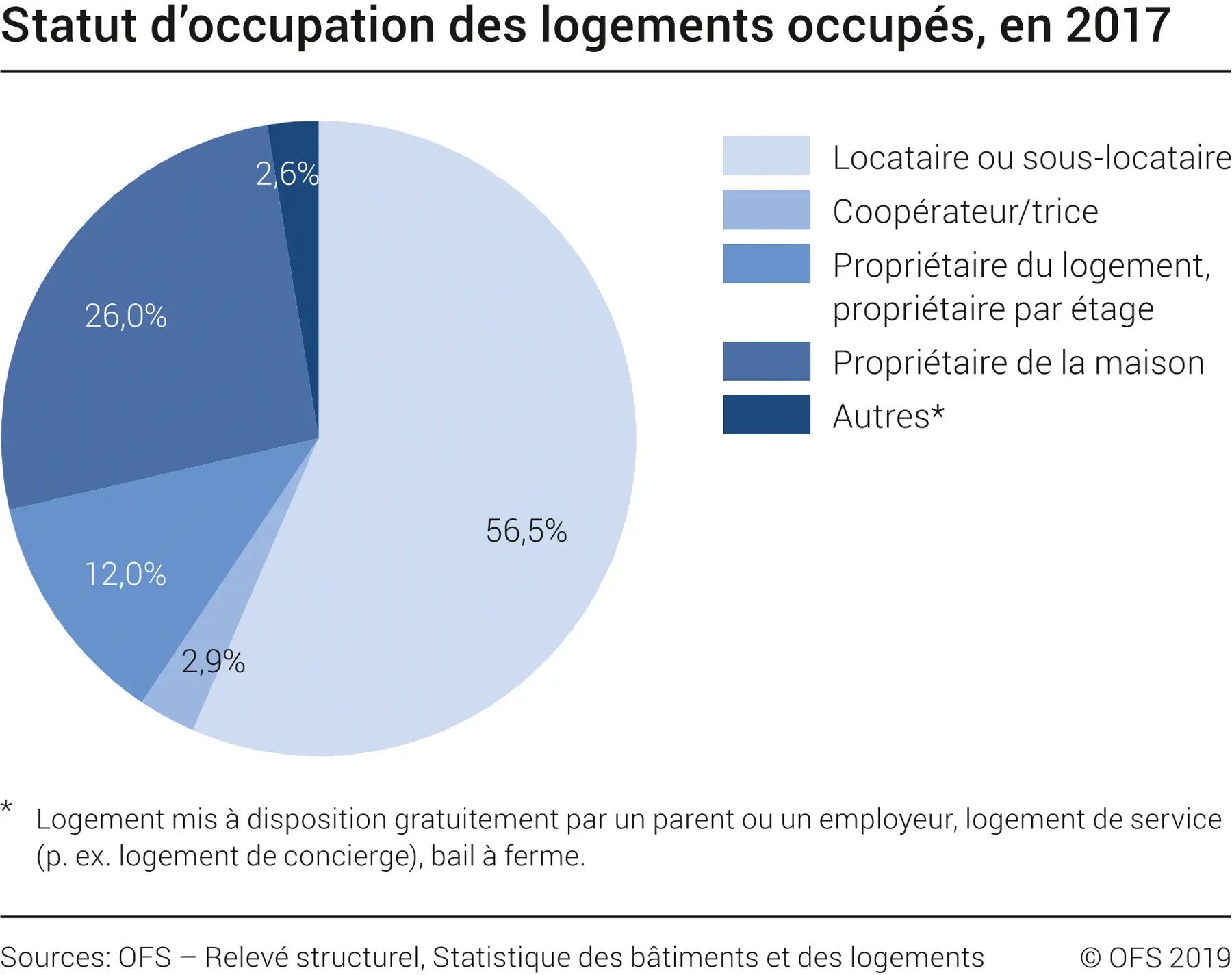

Tenants / owners

The statistics on tenancy status describe whether a private household occupies its dwelling as a tenant, owner or, for example, as a tenant-farmer or usufructuary. The analyses carried out relate to the characteristics of households and dwellings.

Home ownership is increasingly becoming a privilege in Switzerland

Buying property is becoming increasingly difficult in Switzerland despite low mortgage rates. A study published by Raiffeisen highlights, in particular, prices that continue to rise.

Mortgage rates have hit record lows, with ten-year interest rates sometimes falling below 1%. Buying a home should therefore be easier today. However, several factors are thwarting the plans of potential buyers.

The first is the price of houses and flats, which continues to rise across all regions of Switzerland. It fell slightly in the second quarter of the year compared with the first, but rose by 5% compared with the second quarter of 2018.

This is the result of limited supply and sustained demand.

Another obstacle stems from regulatory restrictions:

buyers must have equity amounting to 20% of the purchase price, of which a maximum of 10% may come from the second pillar.

However, only a minority of the population meets these conditions, regardless of the canton.

The proportion of potential buyers is lowest in Geneva and highest in the canton of Uri.

The prospective owner must also be able to comply with the golden rule that housing costs should not exceed one-third of income, with the calculation still having to be based on a very high debt-to-income ratio….

All these barriers are reflected in the home ownership rate, which is currently falling: only 44% of households currently own their own home.

Three out of four Swiss families dream of owning a home

According to a study by Swiss Life, Swiss families still dream of buying a home. But a large proportion of the middle class cannot afford such a purchase, particularly in regions such as Geneva.

Despite often high purchase prices, the Swiss dream of becoming homeowners. According to a study published by Swiss Life, nearly three-quarters of families currently renting are planning to buy a home within the next ten years.

This desire is driven “by the prospect of greater freedom of choice and often also by lower costs”, explains the pensions specialist.

Swiss Life points out, citing Eurostat, that with a home ownership rate of 43%, Switzerland has the lowest rate in Europe in this regard.

Out of reach for many

Although many Swiss people dream of living “in their own home”, this ideal often remains out of reach for a large part of the middle class, particularly in highly sought-after or densely populated regions such as Geneva, as demonstrated by previous studies.

To better understand the continent’s lowest home ownership rate, it is also important to consider the current problems facing pension funds and the risks ahead.

Pension funds: the vested benefits scheme is in serious trouble

Rising unemployment is increasing pressure on the vested benefits foundations, where the assets of the unemployed are held. The Supervisory Board for Occupational Pensions is sounding the alarm

The unemployed face a double blow. Not only does their income fall, but their future pension will be reduced. They continue to pay contributions for cover against the risk of death and disability, but they cannot make savings contributions.

When they leave their company, they leave their pension fund and their assets are placed in a vested benefits account until they find a new job. This system is little known to the general public. But today, the survival of the vested benefits foundations is under threat, Manfred Hüsler, director of the secretariat of the High Supervisory Commission for Occupational Pension Provision (CHS PP), told the press on Tuesday.

What is at stake for policyholders?

Why are the risks increasing?

Vested benefits institutions manage CHF 55 billion, spread across some 2 million accounts. This money is parked there, but the insured person cannot make contributions to it even if they wished to.

The problem of negative interest rates

The need to turn to a vested benefits foundation arises when an employee moves abroad, to manage savings intended for the purchase of a home, or to meet the needs of self-employed people not affiliated to the mandatory occupational pension scheme.

Many vested benefits foundations are backed by a bank or an insurance company and offer a good level of security, according to an expert. However, independent vested benefits foundations cannot rely on any such institution, meaning that if they go bankrupt, all assets are at risk of being lost.

“The worsening economic situation and the persistence of negative interest rates are likely to lead more and more of these foundations to withdraw from the market and, in the worst-case scenario, to liquidation,” warns Manfred Hüsler. Vested benefits institutions will receive increasing amounts of money due to the labour market situation, but they cannot benefit from it. By their very nature, as insured persons are only there temporarily, they invest the funds in short-term instruments at negative rates, but the law prohibits them from passing this impact on to the insured, according to the CHS PP.

Given the difficulty in being accepted by vested benefits foundations, the unemployed are turning to the Substitute Institution (IS), a non-profit organisation acting on behalf of the Confederation. The IS is obliged to accept them, but on unfavourable terms as these are at the legal minimum. It managed CHF 14 billion at the end of 2019. The IS is also suffering from negative interest rates, which the law prevents it from passing on to policyholders, says Catherine Pietrini, vice-president of the CHS PP.

A quarter of pension capital underfunded

On Tuesday, the supervisory authorities also criticised the level of conversion rates, which they deemed “too high” and described as the “predominant risk of the second pillar”, according to Catherine Pietrini. The rate of 6.8% is unsuited to the financial and demographic conditions. This results in a redistribution effect from active insured persons to pensioners, amounting to CHF 7.2 billion in 2019.

The economic crisis has hit pension funds hard, even though they were relatively well prepared, according to Vera Kupper Staub, chair of the CHS PP. Value fluctuation reserves, which are necessary to weather a stock market crash, stood at 65% of the target value at the end of the year.

At the end of April, a quarter of pension capital was in deficit, compared with 1% at the end of 2019. Despite the scale of the economic damage caused by the pandemic, the coverage ratio stood at 105.6% at the end of April, compared with 111.6% at the end of last year.

Bold and responsible property developers are challenging this gloomy picture

A very bleak picture for private home ownership in Switzerland…

…Nevertheless, there are developers who genuinely want to enable the Swiss middle class to become homeowners and even allow micro-investors to invest in income-generating property.

Horizon Dorigny - Complex C

HORIZON DORIGNY is a magnificent example of a large-scale, sustainable and eco-friendly development:

This mega-complex comprises eight buildings – namely, 4 x 7-storey and 4 x 3-storey blocks – complemented by four street-front arcades housing offices and retail units.

Three buildings are intended for rental by the investment fund of a major Swiss bank (600 units) and one for sale on a flat-by-flat basis through ServiPier (200 units).

The surrounding area’s rich biodiversity and easy access to public transport and the motorway are the key strengths of this new residential development.

This is evidenced by its future 1,000 m² fitness centre and high-quality outdoor facilities: water features, a restaurant and a wooded park covering over 6,000 m² form an integral part of the development, as does its 400-seat multi-purpose hall (capable of hosting theatre performances, workshops and other professional conferences).

Residential

architecture Designed today, built to last tomorrow

Set on a site with views of Lake Geneva and the Alps, ‘Horizon Dorigny’ champions a residential architecture that is carbon-neutral, sustainable and designed to foster human interaction, thereby encouraging socialising and soft mobility.

The neighbourhood is therefore entirely structured around pedestrian streets and squares.

It is complemented by a large underground car park offering over 200 parking spaces for the building dedicated to freehold flats.

A visit to the development’s website provides a clear understanding of the project, which offers the opportunity to purchase properties such as a “30m² loft” from CHF 350,000 with just 10% equity… One immediately grasps the appeal of such an investment

Horizon Dorigny - Building C-Prime Loft 30 m²

Sources:

https://www.20min.ch/fr/story/deux-suisses-sur-trois-vivent-dans-une-location-476066536434

https://www.letemps.ch/economie/covid19-lamine-reserves-caisses-pension